The Memory Bottleneck Behind The AI Capex Supercycle

Every GPU cluster in the world depends on one thing many investors are ignoring.

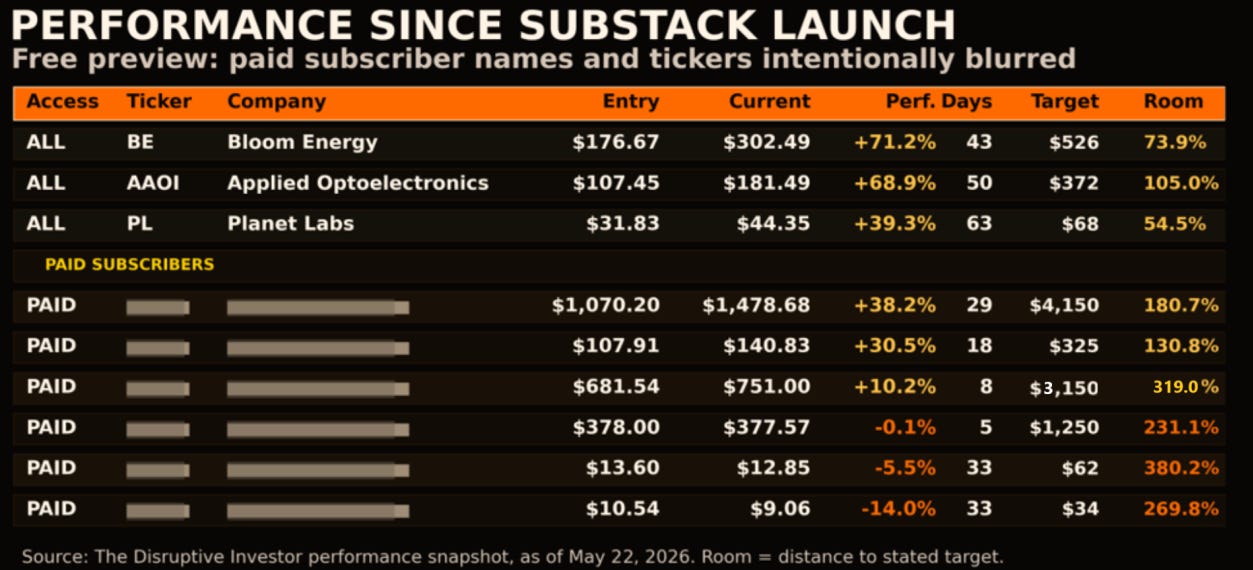

Before the following deep dive, take a moment to look at the performance generated on The Disruptive Investor since the Substack launch ten weeks ago.

The point is not to celebrate a hot streak. It is to show the operating discipline behind the process: entry prices, current prices, days since trade implementation, and the distance still left to price targets.

Paid subscribers can see the full open-trade table after the paywall.

The $1.1 Trillion Capex Wall Is The Real Starting Point

The debate should not start with a ticker, a valuation multiple, or even a quarterly beat.

It should start with the attached exhibit.

Morgan Stanley’s latest hyperscaler capital expenditure (capex) framework is brutal in its simplicity: the five largest AI infrastructure spenders are now expected to move from $261B of capex in 2024 to $805B in 2026 and $1.116T in 2027. That is not a normal procurement cycle. That is an industrial arms race.

The important part is not only the number. It is the timing.

Hyperscalers do not wake up one morning and buy hundreds of billions of dollars of AI infrastructure on impulse. They secure power. They reserve GPUs (Graphics Processing Units, the chips that power AI model training and inference). They build data-center shells. They negotiate supply agreements.

And, crucially, they commit capital long before the first invoice from the customer base fully appears in reported revenue.

The chart above makes that point directly. Microsoft CFO Amy Hood is cited just a few weeks ago saying demand continues to exceed supply. Amazon CFO Brian Olsavsky is cited describing capex commitments made with high confidence in already secured customer demand, often six to 24 months before the first invoice.

In other words, the supply chain is being asked to fund, reserve, and scale capacity before the revenue is fully visible.

That matters because AI infrastructure is not a single product. It is a stack. GPUs sit at the center, but GPUs are useless without networking, power, cooling, storage, and memory bandwidth.

The bigger the capex wave becomes, the more the bottleneck shifts from “can we buy accelerators?” to “can the whole system feed those accelerators fast enough?”

There is a raw material that artificial intelligence consumes every second, but almost nobody sees it.

It does not shine like gold. It does not flow like oil. It does not sit in warehouses like copper.

Yet without it, AI systems slow down. Servers choke. Data centers stop being factories of intelligence and become buildings full of heat.

For decades, Wall Street treated this raw material as a commodity. In good cycles, prices rose, margins expanded, and investors dreamed of a structural rerating.

Then supply came back, prices fell, margins disappeared, and the market swore it would never be fooled again.

That was the old cycle.

Artificial intelligence has cracked it open.

The demand is no longer coming only from traditional information technology markets. It is coming from machines that need more bandwidth, more capacity, and less distance between compute and data.

In AI, speed is not only about the chip that calculates. It is about how much data can be fed to that chip without interruption.

And supply cannot respond instantly.

Clean rooms must be built. Equipment must be installed. Processes must be qualified. Yields must be validated. Customers must secure capacity years in advance.

Capital can move fast.

Industrial capacity cannot.

That delay between demand acceleration and supply response is where the opportunity lives.

The question is not whether the current cycle is powerful. It is.

The real question is bigger:

Is this still a cyclical commodity business enjoying a temporary shortage, or is it becoming a strategic layer of AI infrastructure?